The private sector is not making investments.

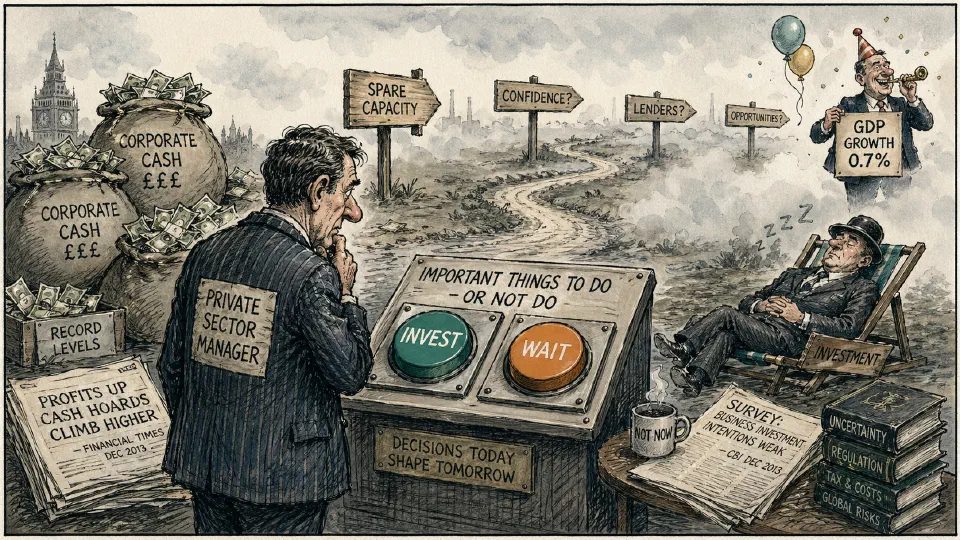

There is not a shortage of cash in corporate balance sheets. No one seems to be sure of the reasons for reticence. Lots of spare capacity? Little confidence in the future? There is still difficulty in finding lenders? It is almost impossible to find worthwhile opportunities? Overall growth of gross domestic product (GDP) is starting to make satisfactory political progress. Investment disappoints. Speculation by private businesses during twelve months to mid-2013 was at lowest since the 1950s. Remuneration packages for senior executives over the last twenty years might be the real culprit. Options based on share price of a company have become a large component of pay. Participants can become rich. Chief executives are at least tempted to manage the business with an intention to increase short-term profits and the share price. Investment right now reduces profits, so why do it? People adapt behaviour to fit their incentives. We cannot expect to see sustainable recovery until there are changes to these aspects of approval/reward.

Prudent, but painful, decisions.

That’s what Government bravely claims for its behaviour. There is cross-party agreement on issues for attention: capacity on electricity, Heathrow airport, national debt and deficit, National Health Service, pensions, and roads and rail. Plus others. They have been kicked down the road. Our chancellor, George Osborne, and his predecessors preferred small, short-term and messy actions. Economic indicators told Mr Osborne to spend in 2010 and promise certain austerities on the arrival of recovery. He knew nobody would believe him. And a squeeze during the run-up to a general election in 2015? This is too much to ask of ambitious ministers. Surprise electors and awaken the journalists. That is an imperative right now. We live in what we call a democracy. It’s the politics stupid.

Culture?

The financial crash in 2008 came as a tremendous shock to the City. Because of the Square Mile’s influence, managerial good may well come from this hammering of arrogance. Organisations which realise the unexpected can happen will see the importance of a determination and capacity to react. It is not an accident that everyone in some firms knows what the business is doing, its priorities, and where it is going. There are 1,001 decisions managers have to make without asking for permission from their seniors. If they know why they are in the game, mistakes are less likely. Don’t hitch the racehorse to the plough. Managers have to recognise that entrepreneurs are likely to be a troublesome lot. They tend to do things then ask. They cross boundaries and take initiatives. They have failures also. But you should be betting on the person, not on one or two ideas.

Prevention of static.

Managers who are anxious about communications often clog-up the works with noise. Other times, they do not listen or give information which either baffles recipients or makes them defensive. One sign of trust in a relationship is appropriate silence.

Here’s a thought from Moscow.

‘I can’t stand this proliferation of paperwork. It’s useless to fight the forms. You’ve got to kill the people producing them.’ Vladimir Kabaidze, Ivanovo Machine Building Works, Moscow (in Fortune).

Experience shows

‘Meetings are indispensable when you don’t want to do anything.’ J K Galbraith, economist, diplomat and writer.