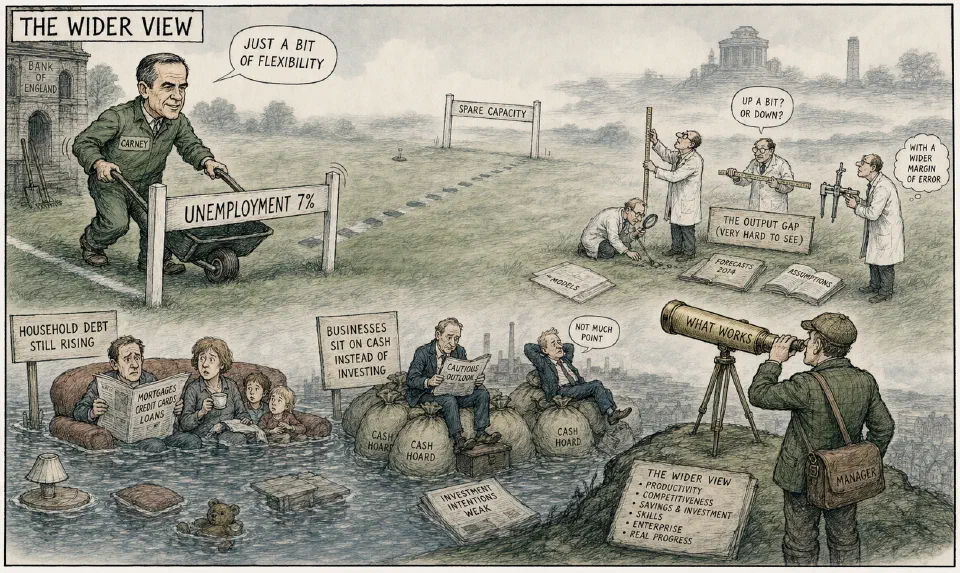

Mark Carney, the Bank of England’s governor, has dumped his ‘forward guidance’ and moved the goalposts.

He told the nation last summer that the Bank would consider higher interest rates only when unemployment fell to 7%. This figure seemed a long time away. However, a rapid rebound in the economy has seen the number of jobless fall quickly and is already close to 7%. Mr Carney says the Bank will measure ‘spare capacity’ now – the amount of slack in the economy. This approach determines how fast it can grow without causing inflation. We were told also about an upward estimate for growth of gross domestic product (GDP) in 2014, from 2.8% to 3.4%.

There are reasons for concern. The Bank knows prediction of unemployment is difficult. The output gap (spare capacity) is more unpredictable and notoriously tough to quantify. Current estimates of its size range from almost zero to 6% of GDP. The information is essential to the outlook for inflation. If it is small, demand in the economy is nearly matching supply, so growth will bring pressure towards higher inflation. Plenty of capacity left under-used by the recession gives flexibility without inflation. As MoneyWeek has noted, studies indicate recessions after financial crises tend to wipe out a lot of capacity. The mistaken investments caused by loose credit are killed-off. City AM reckons another boom and bust period ‘is all too possible’. Mark Carney will need all his skill and care.

Is an economist a scientist?

You know the definition of such a claim, ‘Systematic observation, measurement and experiment and the formulation, testing and modification of hypotheses’. There are doubters relating to this group of practitioners. Economists have had a long period as respected commentators and forecasters on all issues associated with managing the UK … and the world. There has been a premise of training and a profession. In the five years since the collapse of Lehman Brothers, these prominent and self-appointed experts have had an uncomfortable spotlight on their inner workings and assumptions. There are now assertions there is something fundamentally wrong with the structure of western economies. In addition to the financial crisis, the world faces rising inequality and pressing issues of sustainability. Maybe we ought not to be surprised by people’s conclusions that economists have got it all awry? Even Robert Peston (BBC) has said there is a mystery about Britain’s recovery. The Office for Budget Responsibility (OBR) suggests survival is driven by households spending more than expectations. This is happening at a time when real disposable income has gone down and living standards have fallen for most families. Homes are in debt at 140% of available revenue. Five to nine million families would struggle to keep their heads above financial water if interest rates rise to normal levels. The OBR’s predictions for GDP’s growth rely on continued reduction in personal savings and rising liabilities. Does this make sense when businesses have not followed consumers’ lead, and sit on their cash rather than invest?

Some say any recovery is OK, so shut up. But is a binge of credit the road to recuperation we need? So, back to the activities of economists. Some insist we should concentrate on the big picture – the importance of institutions, regulation, distribution of income, central taxes and so on. This is essential before the studies of individuals and markets (microeconomics). But the overview does not direct us to effective action. Despite centuries of study, there is no agreement on such basics as what causes recessions, or how to prevent them. There are some simple and unglamorous matters that do work, but demand persistence. We might be wise to follow physicists and teach/do those things that work.

A different breed of chief executive?

Companies amend their strategies to fit the marketplace. The job of chief executive changes too. A top manager once spent years at a company operating one aspect of the business. This is no longer good enough. Today’s senior executives have to be fast, nimble and adaptable. They need a range of skills way beyond a business degree. The search is for global mindsets and international experience. Continental Europe is a good place to find them. It will soon be commercially dangerous to regard the rest of the world as ‘foreign markets’. Working in other countries used to be dangerous. It kept one away from the corridors of power and sponsors. The base at home is now less crucial as companies independently manage several operations simultaneously. More managers than ever before are hands-on. They get out of the office to do the moving around once delegated to other people. The new technologies allow travel and daily management.

And so say all of us.

In Summer Lightning, PG Wodehouse dubs Lord Emsworth’s secretary as ‘the efficient Baxter’. ‘We have called Rupert Baxter efficient and efficient he was. The word, as we interpret it, implies not only a capacity for performing the ordinary tasks of life with a smooth firmness of touch, but in addition a certain alertness of mind, a genius for opportunism, a genius for seeing clearly, thinking swiftly and Doing It Now.’

That’s it.

‘Any activity becomes creative when the doer cares about doing it right, or better.’ John Updike (1932) – prolific novelist, poet and critic.

Opportunities

‘When one door of happiness closes, another opens; but often we look so long at the closed door that we do not see the one that has been opened for us.’ Helen Keller (1880-1968), American author in We Bereaved.