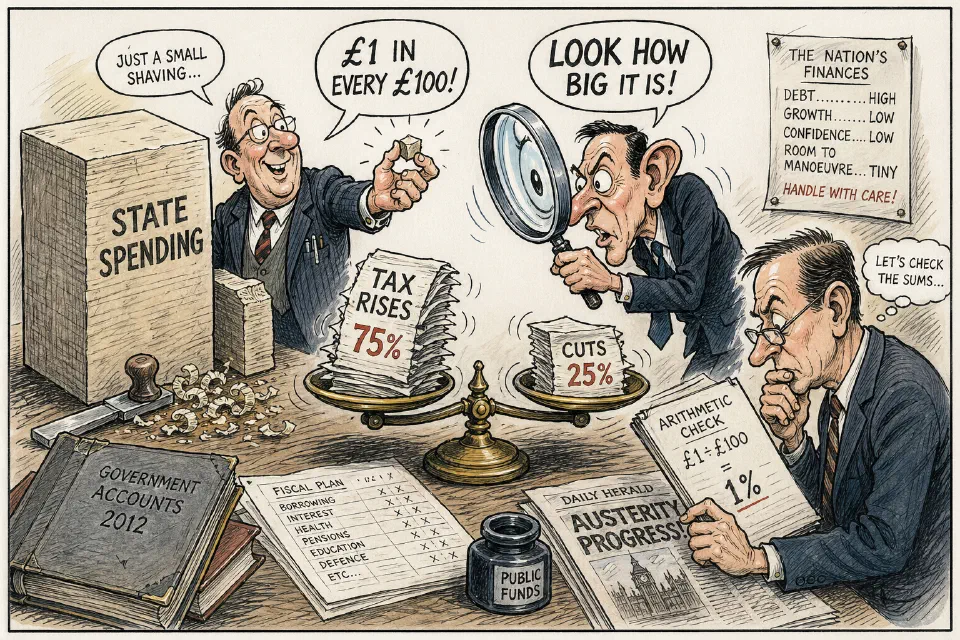

‘At best, the supposedly huge cuts in spending delivered by this government amount to little more than £1 in every £100’, says Tullet Prebon’s Tim Morgan.###

Spending by the State grew in 2009/10 and 2011/12. There was finally a fall in 2011/12, but only by 1.5%. Even then, total spending in the last fiscal year was £22.6bn or 2.4% above 2008/09. And the deficit? It was cut from £161bn in 2009/10 to £123bn in 2011/12. 75% of that £38bn came from higher taxation and only 25% from cuts. Taxes have gone up by £30bn since 2009/10, absorbing 75% of the entire period’s £40bn rise in GDP. The private sector remained on 25% of the already tiny increase in GDP of the previous three years. Morgan reckons the UK has been trying to ‘dupe’ bond markets by combining ‘spin with minimum substance’. If he is right, we have been having the wrong kind of austerity. Thanks to Allister Heath, City AM.

Is there a gravy train of executive pay?

If so, is it grinding to a halt? Alex Brummer and Ruth Sutherland (Daily Mail) accused that the ‘supine attitude of big shareholders’ has helped to create ‘the most cosseted and grasping generation of bosses ever seen in this country’. And shareholders are waking up to the fact that ‘pay for performance translates too often into pay without performance to match’. So what caused the interventions? Two primary reasons. The written media are sure there are good stories. Second, institutional shareholders own investors have taken a deep interest in the matter and threatened to withdraw their funds. Many commentators began to suspect the buoyant markets had become bad for competent governance; only the worst excesses had been stopped. Jonathan Guthrie in the Financial Times reckoned, ‘the genie of executive pay reform is well and truly out of the bottle’. Things have started to happen. Andrew Moss, chief executive at Aviva, stepped down two weeks ago, after shareholders voted against his pay package. High rewards for poor results prompted the departure of Sly Bailey from Trinity Mirror and Astra Zeneca’s David Brennan. There have been substantial protests on this issue at Barclays, William Hill, Immarsat, Prudential, WPP and Xstrata. Plus others. One wonders if these pressures will move to the public sector. Capitalism won the economic argument. Maybe a social mission is the urgent next step?

Wonga is a controversial lender of instant money

and has announced its intention to start a service for small businesses. Watch out for the impact upon this particular market. There are few sectors needing new approaches more than finance for small firms. It has become moribund. Of course, there are legitimate complaints about this intervention by Wonga. But it has been joined by others; Funding Circle and Thin Cats come to mind in making direct connections between borrowers and lenders. Nonetheless, it is clear the government has devised endless enquiries and initiatives and nothing much has happened. The City seems to have lost interest and the clearing banks are in retreat. Wonga might well cause positive changes for owner-managers.

The International Survey Research (ISR) studies once constructed a framework for effective leadership.

Driver is the summary:

- D direction providing an overall sense of quantitative and qualitative goals and objectives

- R respect respecting employees’ concerns and well-being, and regarded as making fair decisions

- I inform keeping employees in touch with plans and performances

- V values articulating clear values and showing integrity in day-to-day management

- E energy moving quickly and flexibly, responding to the market and energising the business

- R role model leaders are watched more than they realise. They have to show positive personal standards.

McKinsey Quarterly Online said that mental traps restrict the ability of senior managers to create a high-performance business over the long-term.

But five characteristics make for corporate strength. The first is resilience – being prepared for potential risks. Number two is executive – the ability to get the basics right, make effective decisions and perform essential tasks. The remaining distinctive features are alignment – pulling the staff into a single vision; renewal – the capability to invest in new markets than can stretch competence and assets; and, complementarity – bringing assets, processes, relationships and managerial practices to act in concert.

Sounds accurate.

‘There exist few modern circumstances where the removal of the word ‘strategy’ from any passage containing it fails to clarify matters, usually demonstrating the argument’s circularity.’ Matthew Parris, quoted in The Times.