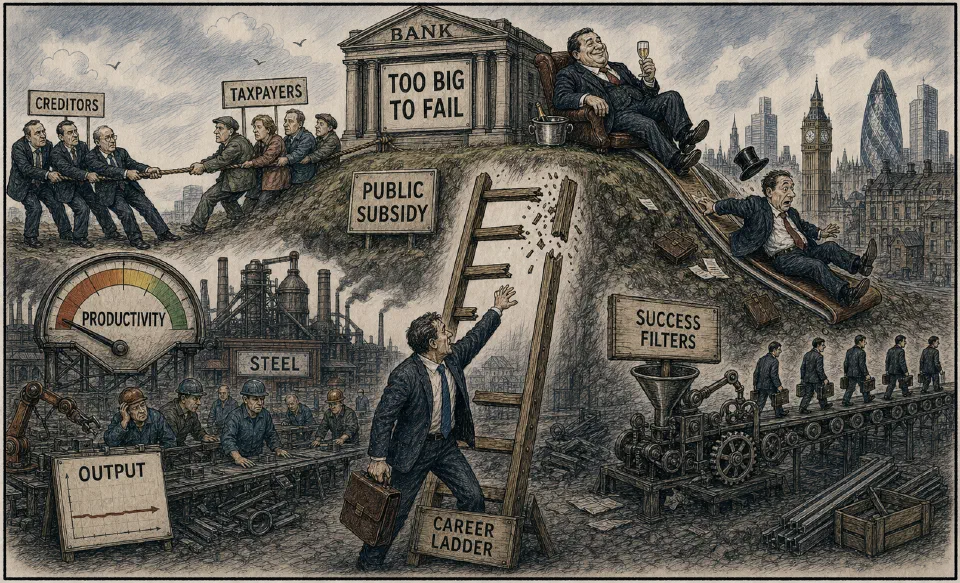

A worry. Too big to fail.

The Financial Stability Board is chaired by Mark Carney, governor of the Bank of England. It advises the G20 group of countries and has said that the world’s thirty biggest banks should raise up to $1.2 trillion in loss-bearing debt, in addition to their equity capital. The goal is to make creditors liable for a bank’s failure, rather than taxpayers. The proposals recommend that a bank would fund at least 18% of its risk-weighted assets with such a debt and equity by 2022. Mr Carney said that the plan would ‘support the removal of the implicit public subsidy’ of banks that are ‘too big to fail’.

Productivity and?

Forecasts for the UK’s economy indicate that a growth will be anywhere between 2% and 2.5% this year and slightly above the higher end for 2017. HM Government continues to tell us things are tough, but with defined reform and hard work we can expect the economy to move ahead. Against this background, including Tata and steel, Markit’s Purchasing Manager’s Index registered last month one of its weakest performances in the last three years. Production was flat after February’s seven-month low and according to Markit, any increases in output reflected better inflows of new business.

This is regarded as confirmation of a major problem associated with productivity, units per hour. Registration of motor cars seems to be a notable exception. An offering of solid and practical support to manufacturers must remain firmly on the Prime Minister’s agenda.

Watch your step at the top.

There is a law of marketing fallibility. This says that when a business pauses to enjoy the view from its hilltop is just the moment it will slide down the other side. In ‘Competing with Information’, Xavier Gilbert argued that being better at doing more of the same leads to competing solely on costs. This is a short cut to annihilation. Winners are likely to be those who renew themselves constantly by listening to, learning from and acting on what the weakest signals in their market places are telling them. Businesses are more open to these indicators when they are fighting to deliver stretching targets, even for survival. They know they have to react quickly. But once they make it, all too often their judgement begins to suffer. Success is not a good school. It tends to filter challenges and discourages experiments. Too few firms understand why they have flourished and what they must do to sustain that trading position.

Ladders have gone.

Several analysts have examined the change of jobs by UK’s managers since 1980. They switch employers more often, make more moves sideways and downwards and have fewer promotions. Managers are likely now to be mobile because of necessity. They have to leave. A steady progression upwards is no longer on offer. Managers are finding their skills and careers are obsolete. They have toiled long and had to climb the corporate ladder only to find it pulled from under them. These are permanent alterations to working lives. A ‘career’ will mean the experience of each person, not one path in one industry.

More time.

‘There is no pleasure worth forgoing just for an extra three years in the geriatric ward.’ Sir John Mortimer, English dramatist, novelist and barrister.