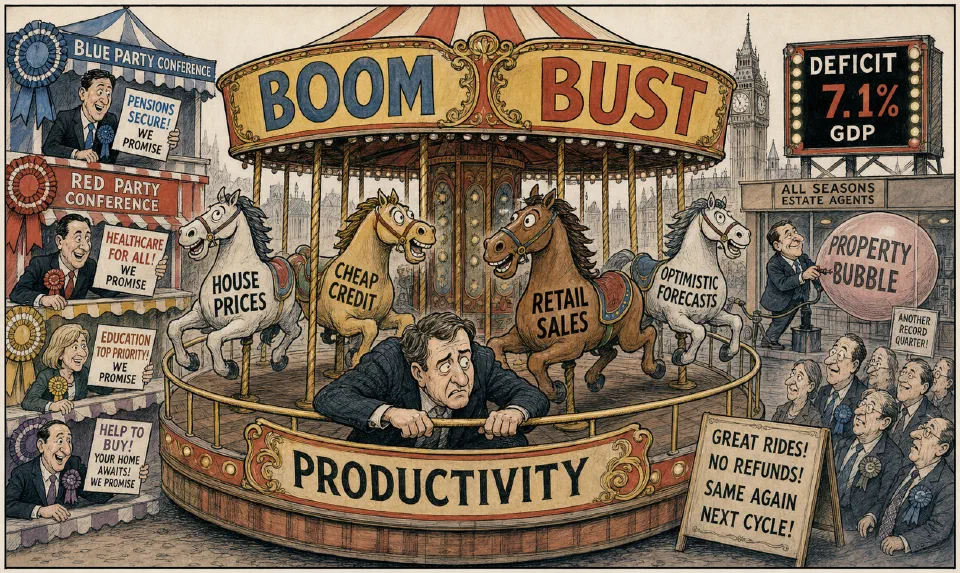

The economy looks brighter than it did last year.

Revised figures in August said the UK’s economy grew by 0.7% in the second quarter of 2013. Optimists are suggesting growth could reach 1% in the third period. The rich countries’ think-tank, the Organisation for Economic Co-operation and Development (OECD), has increased its forecast for our economy from 0.8% to 1.5% this year. Retail sales are holding together and prices of houses in some regions are on an upwards trend. Services and manufacturing sectors are doing better than expectations, and jobs are being created in the private sector. No, we are not experiencing a miracle, but there is cautious confidence. There are some arguments about how long it will last and whether it is ‘good’ growth. The doubts rely upon the knowledge of politically preserved low interest rates, excessive debt and house prices shored up by taxpayers.

We are not out of the woods.

The UK has had a huge deficit for five years. In 2013, the figure will be 7.1% of Gross Domestic Product (GDP). Even with faster growth, it will be 6.5% in 2014. America is at 5.4%, France is 4%. Germany is close to breaking even. Even Greece and Spain have lower shortfalls than this country – 6.9% and 4% of GDP respectively. And the British government is dangerously in debt. It has hardly started the task of getting finances under control. Here we are in the period of annual conferences for political parties. The promises cover pensions, healthcare and education. There is support for buying a house already. The chances are that politicians will not be able to deliver these goodies. We face an imperative to consume less and produce more. Thanks to Matthew Lynn for the ideas.

Reinvention.

The world of business and economics often looks monochromatic. Marks and Spencer was the epitome of British commercial virtues not so long ago. Recently, the company has had difficulty in getting anything right. Much the same seems to have happened at Sainsbury and Tesco is in the queue. General Motors was once America’s most admired company. The revolving door of fashion and favour has turned rapidly for IBM, in, out, nearly back in. The Royal Bank of Scotland and Lloyds TSB have moved from high flyers to dismay. The same is true of national economies. It is not many years since the Asian tigers were dangled before us as exemplars. Those who claimed to see virtues in Germany’s system of industrial organisation are ridiculed today. And what about all those techniques and seminars which attempted to connect us with triumphs of Japan? Corporations have characteristics and personalities, just as humans do. That is why we are inclined to make black and white judgements and why they are so often misleading. Weaknesses are frequently the converse of strengths. Determination can be seen as obstinacy; ambition as arrogance; inventiveness as unreliability; precision as bureaucracy.

The earlier and sustained successes of Marks and Spencer were a testimony to the ability of basic routines in extracting exceptional performances from ordinary people. These methods were effective at securing incremental changes. The demand for improvement was ingrained. Employees did not regard its all-embracing philosophy as a threat. But such organisations find discontinuity difficult because they have created the need for consensus. The keys to success now are speed and initiative for reinventing the business.

As Charles Darwin observed, it is not the strongest of the species that survives, nor the most intelligent. The ones most responsive to change retain life and get new vigour. The Times first listed Britain’s top 300 industrial firms in 1965. Few are still there now. 46% (230 companies) disappeared from the United States’ Fortune 500 in the ‘80s.

Never mind the additions, feel the profit.

Whatever conclusions or comfort you draw from the various predictions and confusing figures on the UK’s economy, recognise the certainty. It is more appropriate than ever to stress margins rather than higher sales. The main issue facing most managers this year is how to profit from little or no growth in their basic businesses.

The problem is that expansion can be, and often is, illusory. It is always patchy and sometimes a result of inflated stock values. At the same time, and more seriously, it all too frequently leads to lax management. So the focus for any business, whatever is happening to growth, must always be productivity – getting more from the same or from less. This is the basic cost of staying in the game.

This seems reckless.

The number of people who now work in estate agents’ offices and the sector makes it the fastest growing part of the national workforce. This situation reinforces fears that the UK is moving towards a dangerous bubble in prices of residential property.

Yep.

‘I don’t make jokes. I just watch the government and report the facts.’ Will Rogers.

And

‘Politics is not a bad profession. If you succeed, there are many rewards. If you disgrace yourself, you can always write a book.’ Ronald Reagan.