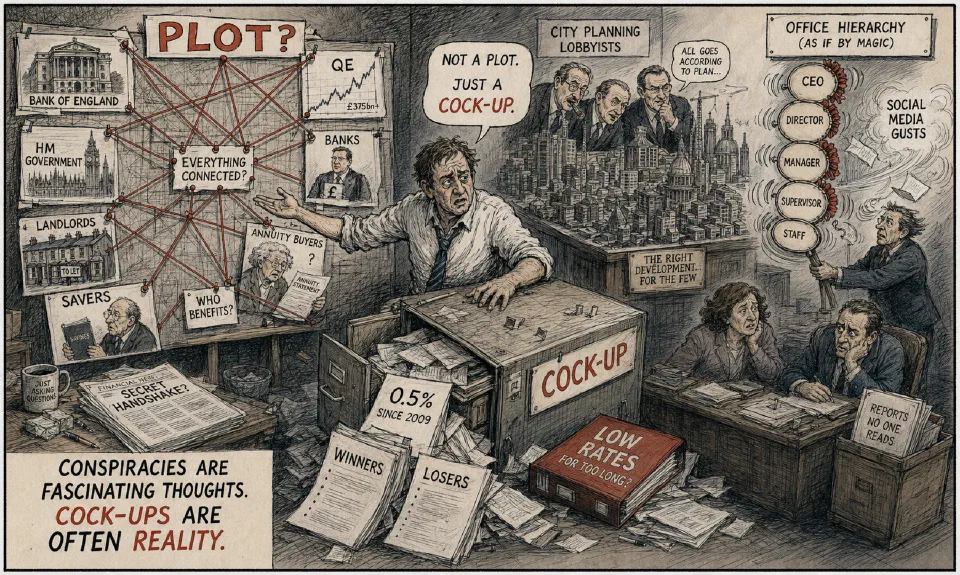

Is it a plot by HM Government?

Unlikely, but between October 2008 and February 2009 interest rates were reduced six times. On 5 March 2009, the Bank of England’s Monetary Policy Committee (MPC) decided on a cut from 1% to 0.5%. This was claimed as an emergency measure, a short-term response to an extraordinary crisis. And five years on, the rate remains at 0.5%. We know that this is the lowest figure since records began in the 1600s.

There have been dramatic winners. They include anyone with a mortgage s/he should not be able to afford, banks, big companies which have been able to take out cheap debt, the growing number of buy-to-let landlords have done well. Many businesses have been kept alive by cheap borrowings. But there have been many losers. Holders of cash (savings) have suffered in real terms (after inflation). Employers with defined-benefit schemes have been in huge difficulties. Low interest makes their future liabilities look higher and higher. The prospects have collapsed for anyone buying an annuity. First-time buyers of domestic property have been hurt by continuing high prices. ‘Normal’ interest rates (inflation plus 3/5%) would almost certainly have corrected the relationship between incomes and cost of property. A major beneficiary is HM Government, the biggest borrower of them all. Its ministers’ constant mantra is reduction of the national debt. The interest has gone down and the Bank of England helpfully buys the debt – this is called quantitative easing. Governor, Mark Carney, has indicated that he expects base rate to be 3% by 2017.

There is a lot of talk about cities.

Those who wish to govern our lives have ambitions, opinions and some influence. Their proposals are imprecise. Cities are the ‘in thing’. How can we make sure that workers and residents in urban developments will benefit? Do they take part in discussions and decisions? There are intensive explorations about hi-tech transport infrastructures, the place of universities, brands, accommodation and bio-tech innovation. It is notable that the ‘big boys’ take a close interest in the activities. Brother, BT, Cisco, clearing banks, IBM, Intel, large practices of accountants and lawyers, local authorities, Peel Holdings, Samsung, United Utilities, Westinghouse and more are there – watching, waiting and lobbying. These are wise things to do. But cities are complex entities. They contain technical, social and physical systems. It takes a long time to overcome an error. The people living in cities outnumber the decision-makers. It is essential to make sure they are not disconnected from the assumption, plans and proposals. By the way, the population of Greater Manchester (ten metropolitan boroughs) is approximately the same as Chicago.

Shake-up of hierarchies.

A report by Accenture predicts that an increasing use of social media will shift the balance of power in organisations and ‘disrupt’ their structures, hierarchies and job titles (the badges of alleged status). Employees will find it easier to create and share information and ideas, and many will grasp an opportunity to define their own learning, career paths and feedback on performances. This is likely to replace conclusions by senior management or centralised departments. LinkedIn’s HR director, Louise Gibney, pointed out in January’s edition of HR magazine that, ‘You only need to look at the number of young people coming into the workplace who use LnikedIn. Last year, we registered 30 million students and graduates on the site – the fastest growing demographic.’ Of course, they will expect businesses to have a presence on social media and to use its potential beyond marketing and messages.

They come and go.

Bill Bonner recorded in MoneyWeek (10 January) that in the 16th century, Spain had the world’s leading currency. In the 17th century, the Netherlands was number one. France’s turn was in the 18th century. The British pound was dominant in the 19th. And in the 20th century, the US dollar was as good as gold. Now we are in the 2000s and a new power has its elbows out. Since 1980, America’s economy has doubled in size per capita. Over the same period, China has grown 13-fold. Will this continue? No. But China’s economy is still growing twice as fast as the US. China is poor and getting wealthier. America is rich and getting poorer. Maybe Africa is the next winner and opportunity?

Process, process!

‘Nothing will be attempted, if all possible objections must first be overcome.’ Samuel Johnson (1709-84). Biographer, poet and lexicographer.

That’s so.

‘In innovation, as in any other endeavour, there is talent, there is ingenuity and there is knowledge. But when all is said and done, what innovation requires is hard, focused, purposeful work.’ Peter Drucker (1909-2005).