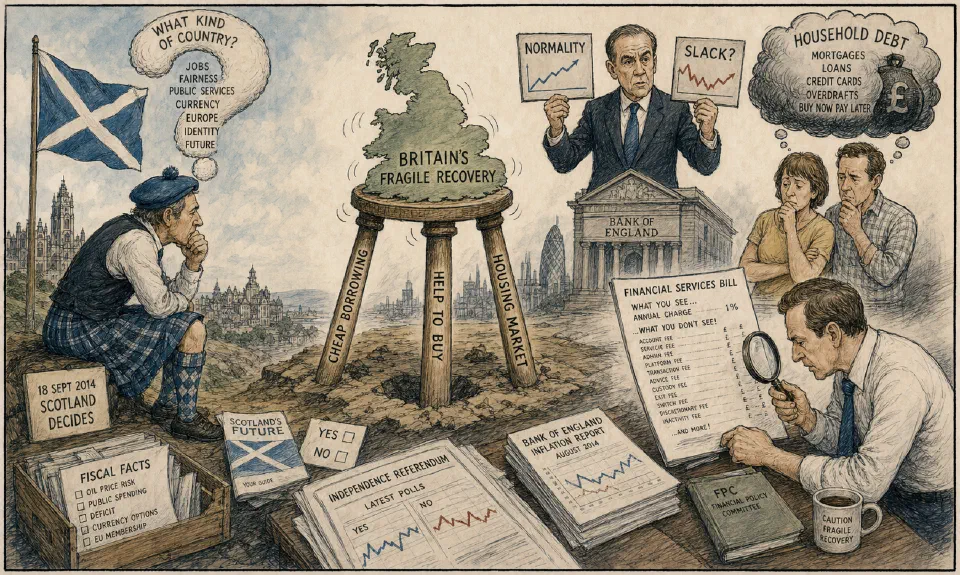

Why the upturn?

A major question is whether the recent economic upturn is due to the austerity measures. Or is it a happy coincidence of falling energy prices, low-cost loans and stimulants to build houses? Is our government repeating the mistakes of the past – a recovery led by the housing market, generated by supply constraints, fuelled by cheap borrowing, and aided and abetted by the Help to Buy scheme? How vulnerable is this to rises in interest rates – quite possibly and for some, unhelpfully, before the next election? It is thought often to be a no-brainer that cutting the government’s deficit reduces the national debt.

However, cutting expenditure reduces demand, particularly by the poor, who spend a larger proportion of their income. This adversely affects GDP and employment. This in turn lowers tax revenues, worsening the deficit. The conclusion is that a government’s investment plans play a key part in increasing demand and hence reducing the national debt.

This may explain why, despite the tough talk, the UK government has still run the deficit throughout the post-recession period. The bottom line is that there has been a lot less austerity than we were led to believe, and austerity is unlikely to have been responsible for the first signs of recovery. Arguably, the fact that government’s outgoings were not cut as aggressively as some would have liked has allowed the restorations to begin. All the same, it is still too fragile and unimpressive to be worth shouting about; and possibly assisted by unsustainable interventions in the housing market. With reductions in benefits and rises in interest rates likely to have an impact down the line, then even this recovery may be in jeopardy before long.

Financial services is a strange industry.

This is the opinion of Morgan Housel. There’s nothing else like it. Is there another sector in which customers have so little knowledge of costs? Most people have no idea what they are paying managers of their monies. Yet if you are moderately wealthy, this might be your biggest outgoing. These practitioners can do much harm, but do not need credentials. Results do not seem to matter a lot. Not many well-paid managers beat what could be achieved in a low-price index fund, but remain in business for decades. Finance is an important service/activity for everyone, yet so few of us care about it. Maybe each of us has a moral obligation to have a basic understanding of how saving, investing and debt work?

Interest rates up?

Anyone expecting a rise in interest rates in 2014 is facing disappointment. Mark Carney, governor of the Bank of England, said in the last quarterly report on inflation that Britain’s economy has returned to ‘a semblance of normality’. However, the Bank reckons there is more weakness in the labour market than suggested in earlier comments. It suggests growth in wages will be 1.25% this year, rather than previous estimate at 2.5%. Mr Carney indicated also that even if we eliminated spare capacity overnight in the economy, the appropriate interest rates would be close to the present situation. This is because of high indebtedness of households and the low recovery in the eurozone. Some informed observers have thought for a long time that the Bank is in the dark about the true state of the economy. Moreover, the Bank‘s report said, ‘ …. there is a wide range of views’ in the Monetary Policy Committee about the slack in the system. Measurement in this context is an imprecise skill. We should have learnt from the failure of central banks to do anything about the global financial crisis that they are as clueless as the rest of us.

Experience.

‘There are no solutions, only trade-offs.’ Thomas Sowell, a US scholar on democratic politics, quoted in the Financial Times.

And more.

‘You can’t learn too soon that the most useful thing about a principle is that it can be sacrificed always to expediency.’ W Somerset Maugham, quoted in The Times.