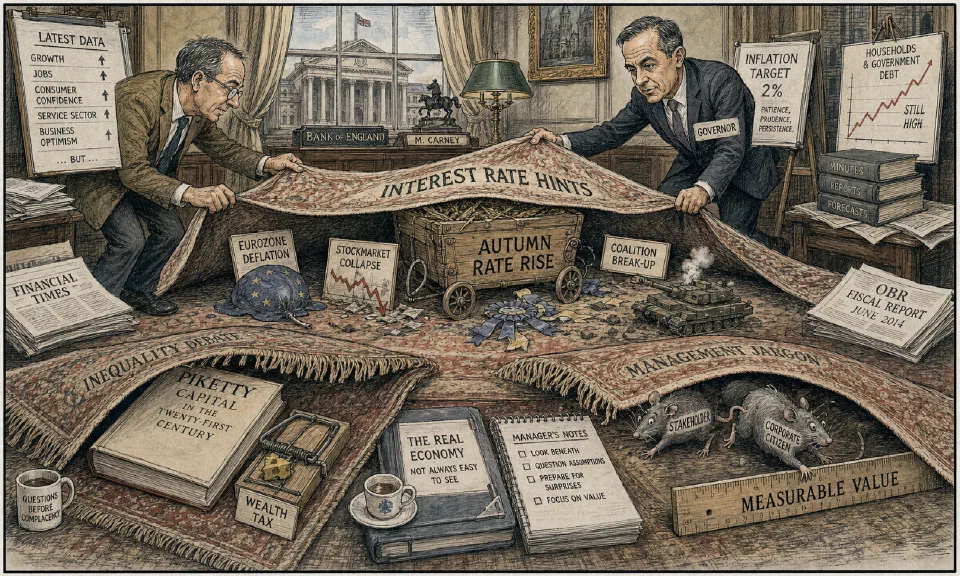

Big hints.

The signals are clear. Mark Carney, governor of the Bank of England, has dropped big hints that interest rates will rise sometime in autumn. This would be the first such move for seven years. Commentators of various persuasions and skills have told us each day that rates will go up soon. Growth is on the way up. Unemployment is falling quickly. House prices outside the South East are on an upward trend. New jobs and additional businesses are being created. The deficit is coming down. Trading confidence is higher. It seems sensible to move rates back to their ‘normal’ levels. After all, the present low interest rate was intended as a response to an ‘emergency’. Where is that crisis right now? The City’s traders have enhanced the pound’s value and lenders have nudged-up their interest rates. Some scope to cut them when the economy turns down again is a good idea.

There will be surprises that could upset this applecart. These might include: (i) falling prices as a result of the eurozone getting into a deflationary spiral; (ii) a collapse in the stockmarket; (iii) a breakup of the coalition government; and/or (iv) a regional war elsewhere. Our central bank is engaged in a new version of ‘forward guidance’. The last one did not last long. In reality, Mr Carney has no more idea than the rest of us what the world will look like in October. Bear in mind how quickly our economic world went wrong in 2008. Managers are wise to be cautious.

An overnight sensation in 2014.

The first volume of Karl Marx’s ‘Das Capital’ was published in 1867. One thousand copies were sold in the next five years. It was not translated into English until 1890 and was almost ignored by the UK’s newspapers and magazines. The Economist mentioned the book in 1907. ‘Capital in the Twenty-First Century’ by Professor Thomas Piketty, a Frenchman, was an immediate hit during March. In the United States, his publication was the top seller on Amazon, including fiction. The right subject at the right time is one reason for this success. Professor Piketty examines the causes and dangers of greater inequality. The Americans had dismissed for years the gaps between the haves and have-nots as a European obsession. However, they have been embarrassed by the excesses of Wall Street and are talking about the rich and redistribution. They are attracted by this book of 577 pages which argues that wealth concentration is inherent to capitalism and recommends a global tax on wealth as the progressive solution. This conclusion has delighted the left, infuriated the right and stimulated discussion amongst the inert professional economists. The Economist points to three substantial contributions by Thomas Piketty. He is a pioneer in using tax statistics to measure inequality. He then submits a theory of capitalism that explains these facts and offers a prediction of where wealth distribution is heading. His third outcome is an offering of policies and your scribe feels that the author has ceased a remarkable piece of scholarship and shifted towards unexamined prejudices.

Dangerous notions.

Innovative products are being rolled out by the manufacturers of jargon : ‘stakeholders’, ‘corporate citizens’ and ‘company members’. They will lead to cynicism and bring comfort only to their purveyors. Whose interests ought the corporation to serve? Those of the shareholders and debtholders, who own it? Or those of the employees, who depend on it? These are bogus questions. What matters is how the corporation sets its course to make the greatest contribution to society. The blunt certainties are that the state must eliminate all externalities and managers should act to increase the total value of their businesses. All else is a chimera,. The imperative has little to do with shareholders as such. Maximising value increases the average standard of living, whereas consuming £100-worth of inputs to produce outputs at £90 is the well-trodden road to ruin. A stake in that is useless.

A company which pursues measurable economic performance does not ignore its constituencies. Mistreated employees leave or become less productive; abused suppliers drop quality and timeliness; neglected customers go to a competitor. The present notion of ‘stakeholder’ offers no guidance whatsoever for making decisions. A primary danger is that managers would be turned loose to exercise their whims, idiosyncrasies and personal prejudices. And how would others gauge their results?

Just a thought.

Necessity is the mother of invention but laziness may well be the midwife.

A deadly sin.

Feeding problems and starving opportunities is one of a manager’s deadly sins.

It is astonishing how many companies assign their best performers to problems. These people become devoted to the old business which is sinking faster than forecasts; to the declining product being outflanked by a competitor’s new offering; to the ageing technology. The opportunities are left to fend for themselves. They are the future. They produce growth. They are every bit as difficult and demanding as problems. Maybe a manager ought to draw up a list of opportunities facing the business and make sure each one is adequately staffed and supported? Only then set out the problems and worry about managing them.

How do we get the right balance?

‘Management have been allowed to act like owners, but it is the stockholders who own companies, not managements and the stockholders are just beginning to realise it.’ T Boone Pickens, corporate raider (1985).

Priorities.

‘When a subject becomes totally obsolete we make it a required course.’ Peter Drucker.